COVID-19

What happened?

Resilience

After the Great Financial Crisis (GFC) of 2008/2009, the Basel Committee on Banking Supervision kicked off the post-crisis regulatory reform agenda in December 2010 with its publication of the Basel III standards. The Basel III standard was then implemented in the EU with the Capital Requirements Regulation and the Capital Requirements Directive IV. In 2017, the Basel accord from 2010 was superseded by the BCBS document Basel III: Finalising post-crisis reforms. The final Basel III reforms are now due to be implemented by member jurisdictions by January 2023.

The post crisis regulatory reform agenda, which started with Basel III, has addressed many significant shortcomings of the pre-crisis regulatory framework that were revealed during the GFC. In 2008 and 2009 it became apparent that banks were not sufficiently capitalised to withstand the most severe shock to the financial system since the Great Depression. The effort made by policymakers to shore up the banking system and increase its resilience is also reflected in the development of the regulatory bank capital. Since June 2011, the Common Equity Tier 1 (CET 1) ratio, which comprises capital of the highest quality, increased to above 14% in June 2019 and is well above the minimum requirement of 7%. The situation for the leverage ratio is very similar with buffers currently at more than 5% and thereby standing comfortably above the minimum requirement of 3%. Those figures have also been confirmed by the EBA’s Spring 2020 EU-wide transparency exercise, which reports very similar figures for the CET1 ratio as well as the leverage ratio for end 2019.

The strong capital position of the EU banking sector became an important factor when the Corona crisis hit European banks in Spring 2020. Thanks to the high levels of CET1 capital and the support measures of regulatory and supervisory institutions, banks were able to maintain lending to the economy without having to restrict, excessively, the amount of credit given to customers, a thereby reinforcing the economic downturn.

The situation for the liquidity figures which are equally important for the stability of the banking sector draws a similar picture. After the initial reforms, the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR) have reached levels above the minimum requirement, which for both ratios, is currently 100%. Those ratios are designed to increase the resilience of the financial system by allowing banks, in the case of the LCR, to “survive a period of significant liquidity stress lasting 30 calendar days”, and incentivising banks to seek more stable sources of funding in the case of the NSFR. The strong position for the LCR was also confirmed by the EBA at the outset of the Coronavirus crisis with figures “well above the minimum level of 100%”.

Consequently, the EU banking sector has entered this shock, induced by the outbreak of the Coronavirus crisis, and the following restrictions introduced by governments, designed to limit the impact on public health, in a much better position than twelve years before. Therefore, it is clear that ten years after the first Basel III standards, policymakers, together with the banking sector, have managed to improve, significantly, the resilience that supports banks in managing significant stress on the financial system.

Bank policy reaction

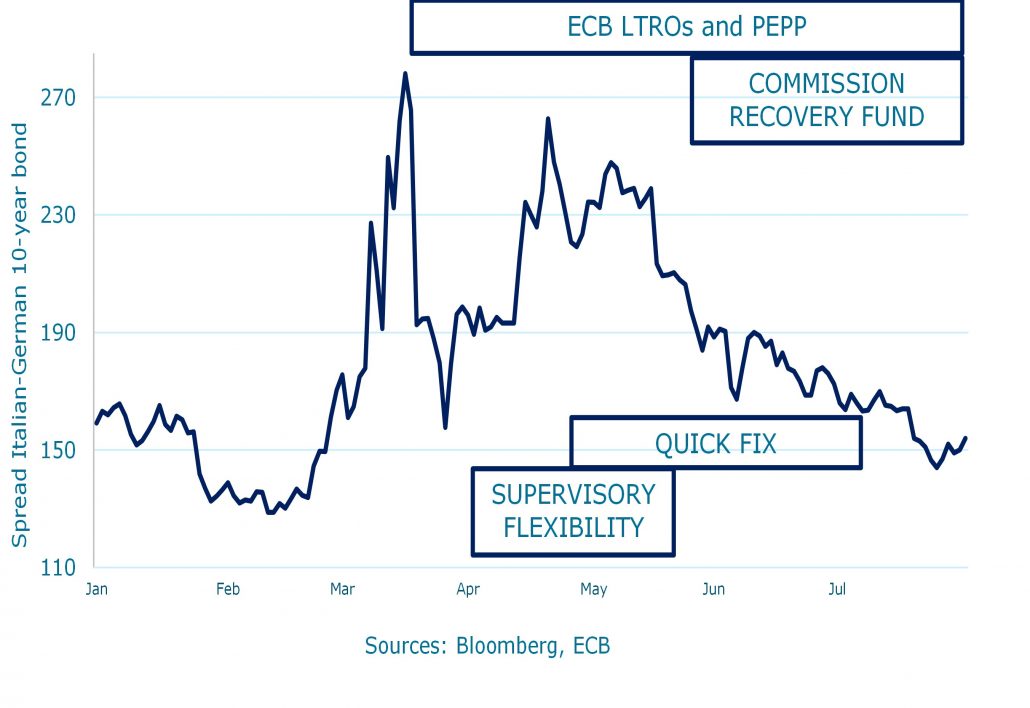

In 2008, after the shock of the Great Financial Crisis the policy reaction was perceived by many as too little and a bit too late. This time around, the response to an unexpected crisis has been firm, substantial, and quick. More importantly, EU authorities have coordinated a combined action plan on the various components of the policy toolbox. As a result, the upsurge in market volatility was quelled in a short time. On monetary policy, the ECB announced a comprehensive package of measures including additional long-term refinancing operations (LTROs) bridging the period from March to June 2020 to provide liquidity at favourable terms in the aftermath of the Covid-19 shock, as suggested by the EBF. The envelope of the Pandemic Emergency Purchase Programme (PEPP) was increased by €600 billion on 4 June to a total of €1,350 billion. On regulatory policy, co-legislators have agreed in a record time on a quick fix that, together with ECB supervisory flexibility measures, have permitted EU banks to keep the level of lending without their capital ratios deteriorating. Rounding off the previous measures, the Commission launched a major recovery plan for Europe including a new recovery instrument of €750 billion with new financing raised on the financial markets.

Banks are now perceived as part of the solution to the health crisis. The maintenance and enhancement of the level of lending is a common objective of banks and authorities for the sake of economic recovery. On 11 March 2020, right after the Covid-19 outbreak, the EBF called on the EU authorities for a coordinated programme to put the EU banking system in the best conditions to withstand the initial shock and keep on serving the economy. That programme was articulated in a series of EBF recommendations on monetary policy, supervisory flexibility and regulatory quick fix, many of which were taken on board. According to EBF estimates, EU banks obtained an average relief of almost 200 basis points from the CET1 ratio, which has been used to absorb the initial impact of the crisis at the 2020 closing and start 2021 without major disruptions to the resilience of the banking system at large.

Altogether, the minimum CET1 capital requirement for the EU banking system has been reduced, on average, to almost 200 bps with the battery of regulatory and supervisory measures adopted by EU authorities. This is allowing banks to keep up the level of lending to the economy.

According to EBF estimates, three types of measures can be distinguished by their nature:

- temporary reductions amount to approximately 70 bps;

- discretionary reductions are up to 25 bps;

- permanent reductions, many of which were anticipated in the CRR3 package which enters into force on 1 January 2021, summing up around 90 bps.

Support the economy

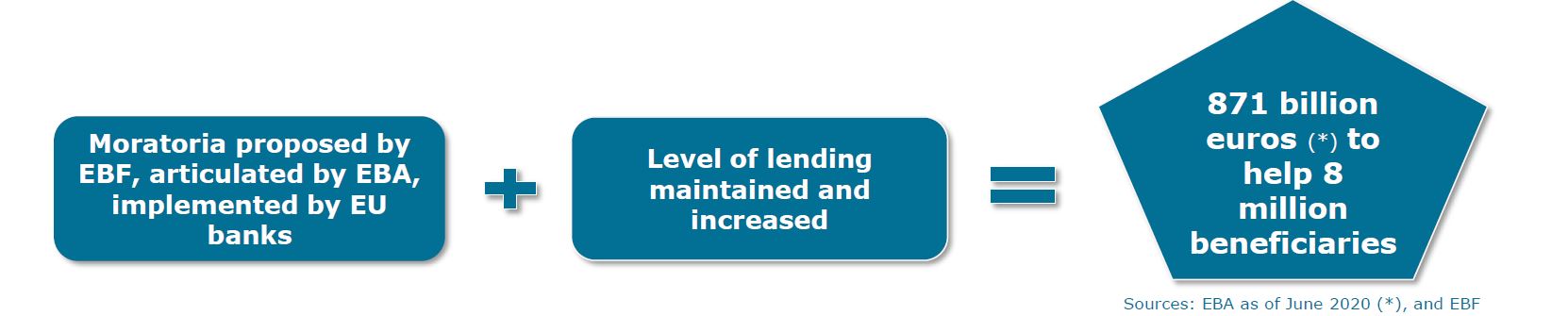

The outbreak of the COVID-19 pandemic has resulted in disruptive effects to the European economy. Many corporates and households are struggling to keep up with their payment schedules of specific financial facilities granted before the pandemic. The banking sector has responded swiftly to the risks and shocks that the spread of the pandemic has brought by rapidly operationalising private and public moratoria schemes under the EBA Guidelines.

Banks are also supporting consumers by further increasing the communication with them especially via digital channels. In this context, the European banks have proved to be part of the solution in dealing with the economic consequences of the pandemic. Such actions permitted European banks to keep fuelling the private sector by providing loans to European borrowers.

Since the launch of moratoria schemes under the guidance of the EBA on 2 April 2020, EU banks have made a huge effort to postpone the payment of loans of clients affected by the crisis. As of June 2020, there has been a significant use of the moratoria tool with payments postponed for an amount of €871 billion, according to EBA, in order to alleviate the pressure of the crisis on banks’ clients. In total, according to EBF estimates, more than 8 million individuals have benefitted from the deployment of national moratoria schemes in Europe. More specifically, more than 5 million households have been able to postpone their payments with the aid of their banks, while more than 2 million companies are also benefitting from moratoria conditions on their loan payments. Overall, more than 85% of the borrowers’ requests for postponement of payment schedules were accepted by the banking sector.

What is next?

Real-life stress test

After the Global Financial Crisis (GFC), stress testing has been an important tool in the supervisory toolkit to assess banks’ resilience to economic stress scenarios. The stress tests are then used by the ECB to assess whether additional measures need to be taken to strengthen the banks’ resilience.

The key features of the EBA’s stress test exercises have been the standardised methodology and the stress scenario defined by the European Systemic Risk Board (ESRB). The standardised methodology is a set of rules used by the EBA and supervisors to define how banks should calculate the impact of the stress scenarios on their institution. So far, the methodology was highly standardised giving little room for banks to use their own models and assumptions. The standardisation which was accomplished by setting out common assumptions to apply to all banks, for example, regarding the characteristics of banks’ balance sheets, was meant as a way to ensure that individual banks’ results were comparable and to prevent banks from being overly optimistic in estimating their own capital situation during a period of economic stress. The other important part of the exercise, the adverse stress scenario from the ESRB, is a hypothetical scenario which envisages a situation in which the banking situation might come under significant stress.

The scenario, which is conceptualised to cover a period of three years, is based on the most relevant financial stability risks to which, according to the ESRB, banks were exposed at the time of its development. For example, for the initial 2020 exercise (in the end, postponed) the ESRB developed a “lower for longer scenario”, “confidence shocks drive expectations of nominal growth significantly below what is currently forecast which leads to a self-fulfilling economic recession in the EU and, commensurately, an ultra low-interest rate environment.” While realistic, for example, the scenarios’ reflection of potential trade tensions and the current low-interest rate environment, the scenario itself remains hypothetical and is not designed to be a “forecast of the most likely negative shocks to the financial system”.

Turning to the current situation of the EU’s banking system, it becomes clear that the EBA’s 2020 stress test has been replaced by a real-life stress test. Because of the postponement of the 2020 stress test, the ECB conducted a COVID-19 vulnerability analysis. The analysis, of which the results are shown in the graph below, was launched in order to assess banks’ resilience to the economic shock caused by the coronavirus. The vulnerability analysis was conducted with Eurozone banks and based on the original EBA methodology for the 2020 stress test, therefore some of the assumptions, such as the covered risk areas or the static balance sheet assumption remain the same. Comparing the outcome of the vulnerability analysis with the last three stress tests, it may be seen that the potential economic shock resulting from the COVID-19 crisis is more severe than the shock assumed in the previous exercises.

For example, as described by the ECB, the COVID-19 scenarios assume a deeper recession than the GFC, even though the downturn is not as prolonged. In the central scenario, the ECB assumes that the current level of capital, which is at 14.5%, depletes by about 1.9 percentage points. The cumulative GDP depletion over the three years (accounting for the rebound after a sharp recession) shows a 0.8% GDP depletion. This is the most likely scenario to materialise according to estimations from the Eurosystem, and currently, the banking system is sufficiently capitalised to withstand this scenario, while “continuing to fulfil its functions, in particular, to meet the demand for lending to the economy”. However, it only takes the adverse scenario, which is “a more adverse, but still plausible development of the crisis”, before a number of banks need to take management actions to mitigate the impact of the crisis, which are not yet considered in the analysis. At the same time, this scenario involves a capital depletion of 5.7%, which is much severer than anything that has been stress tested before, as can be seen from the graph.

Cost of funding

European banks have more than doubled their total capital ratio in the last decade. An important part of the increase has been contributed by the issuance of eligible loss-absorbing own funds instruments such as Additional Tier 1 (AT1) and Tier 2 (T2). This reinforcement of the European banks’ capital base has put the sector in a condition to withstand a major economic shock like the Covid-19.

The trend of market prices of contingent debt instruments gives an indication of how the decisive monetary policy reaction has quelled the markets of bank debt. The spreads of AT1 rocketed up in the sessions following the outbreak in about 1,700 bps from per-COVID-19 levels, with a yield to maturity close to 10% reflecting strong fear sentiment in the market. Tier 2 instruments followed the same increasing trend, offering a yield close to 2.7%.

However, the abundant market liquidity ensured by the ECB asset purchase program and other monetary policy instruments helped reduced volatility and overall bond spreads, calming down the high risk perceived by investors.

However, the abundant market liquidity ensured by the ECB asset purchase program and other monetary policy instruments helped reduced volatility and overall bond spreads, calming down the high risk perceived by investors.

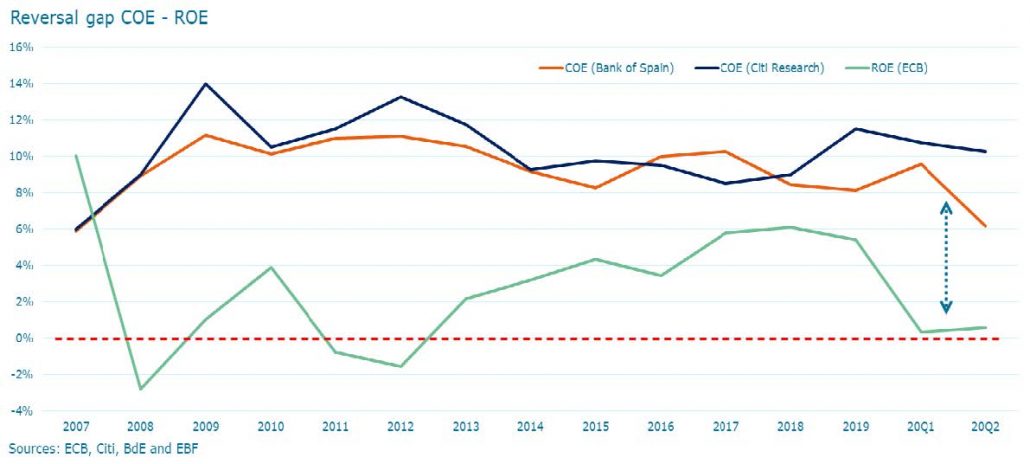

European banks managed to improve substantially their ROE, touching 5.6% at the end of 2019 but still lagging far behind from their international peers. The shock of the pandemic in Q1 2020 dragged down banks ROE to 0.33% with a slight increase to 0.6% in Q2 2020. Meanwhile, the COE is also being reduced in part benefitting for the ample market liquidity. The gap between ROE and COE was narrowing down from 2017, however, it has widened again in 2020. The following graphic shows COE estimates during the last decade using different models by Citi Research (blue line) and in a recent study published by the Bank of Spain (orange line).

Against a background of increasing competition of non-regulated entities operating in the financial system, narrow margins resulting from longstanding low-interest rates and general economic deterioration, the closing of the reversal trend between COE and ROE remains an outstanding issue for the European banking system a pending subject for the future.