“A complete Banking Union is essential for the future of the Economic and Monetary Union and for a financial system that supports jobs and growth.”

“The completion of the Banking Union is about making sure that the European banking sector is one banking sector. We need to make sure that when an investor looks at banks in Europe, they see a European bank – whether they see it from Milan, Frankfurt or Paris.”

“Good supervision is based as much on judgement as on rules. Supervisory judgement is crucial in order to accommodate the individual situation of each bank; it should not be confined by overly detailed rules. In particular, this is crucial in a rapidly changing financial landscape in which rules and regulations simply cannot keep up. Here, we need to thoroughly understand evolving risks within and across banks, and we need to address them by taking a dynamic and forward-looking supervisory approach.”

Supervision

Established platform for the dialogue between banks and the European Central Bank

Banking supervision in the banking union

The EBF supports financial market integration in Europe. The initiative for a Banking Union is instrumental to achieving a more integrated European banking system. The establishment of the ECB Single Supervisory Mechanism is a decisive step that not only affects the supervised banks but also constitutes a point of reference for banks and other supervisors from all over Europe and worldwide.

The EBF supports financial market integration in Europe. The initiative for a Banking Union is instrumental to achieving a more integrated European banking system. The establishment of the ECB Single Supervisory Mechanism is a decisive step that not only affects the supervised banks but also constitutes a point of reference for banks and other supervisors from all over Europe and worldwide.

The EBF has engaged in this endeavour from inception, in 2014. The implementation of the new SSM supervisory culture requires a lot of coordination, timely and effective communication as well as mutual understanding between all parties. In this journey, numerous operational difficulties arise. The EBF collaborates with the ECB in the identification and solution of problems and circumstances that deserve special attention from banks and supervisors.

Informed dialogue EBF-ECB

Pictures from the EBF SSM Boardroom dialogue

Pictures from the EBF SSM Boardroom dialogue

Which issues we discuss with ECB?

Operational issues and strategic themes

EBF scope and activity

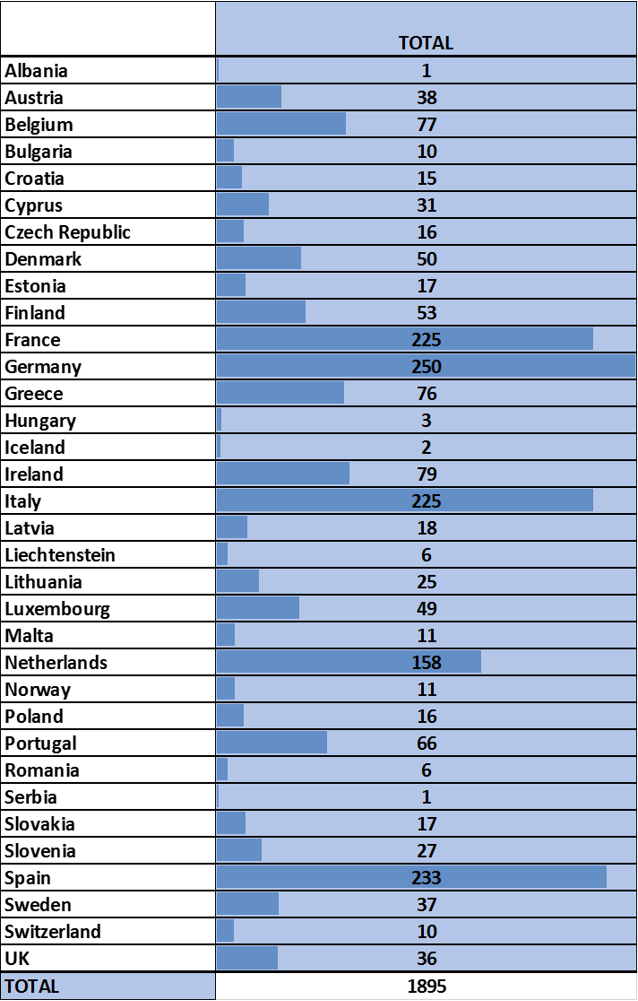

Number of bank participants by country in EBF meetings with ECB in Frankfurt from 2015 to mid-2020